Should You Hedge Your Cattle With Options? A Commercial Producer’s Guide

If you run cattle long enough, you learn the market doesn’t care about your breakeven. It will hand you a profitable price one week and take it back the next, and the producers who survive the down years aren’t the ones who guessed right — they’re the ones who had a plan to protect a price they could live with. Options on cattle futures are one of the most flexible tools for building that plan, because they let you set a floor under your selling price, or a ceiling over your buying cost, while keeping the chance to do better if the market moves your way. As a buyer, the premium you pay is the most you can lose. Hedge cattle with options!

It starts with the decision most producers are actually wrestling with: protecting a price without giving up the upside or draining the operating line. From there, it moves, in clearly marked sections, into the implementation realities that separate a hedge that works from one that gets abandoned after the first margin call — contract sizing, expiration, volatility timing, spreads, the risks of selling options, hedge accounts, and how SPAN margin actually behaves. It treats options as a form of commercial risk management, not speculation.

Key Takeaways for Cattle Producers

- A put sets a price floor on cattle you’ll sell; a call sets a ceiling on feed or feeder cattle you’ll buy. As a buyer, your maximum loss is the premium — full stop.

- For most family cattle operations, a put is often easier to live with than a short futures hedge, because there are no variation margin calls draining the operating line on a rally.

- Options keep your upside. If the market runs, you let the option go and sell (or buy) in the cash market, out only the premium.

- The premium is real money at risk. If the market never reaches your strike, the option can expire worthless. That’s the cost of a known, bounded outcome.

- Contract sizing is a fundamental decision, not a footnote. Live cattle contracts cover 40,000 pounds and feeder cattle 50,000 pounds, yet most herds don’t divide evenly into those units.

- Your lender cares about this. How you hedge changes your working capital, your margin exposure, and whether your account qualifies as a bona fide hedge account — all questions a banker will ask.

The Decision Behind the Decision: Protect a Price, or Protect Working Capital?

Every cattle marketing decision looks like a question about price. It’s really a question about working capital.

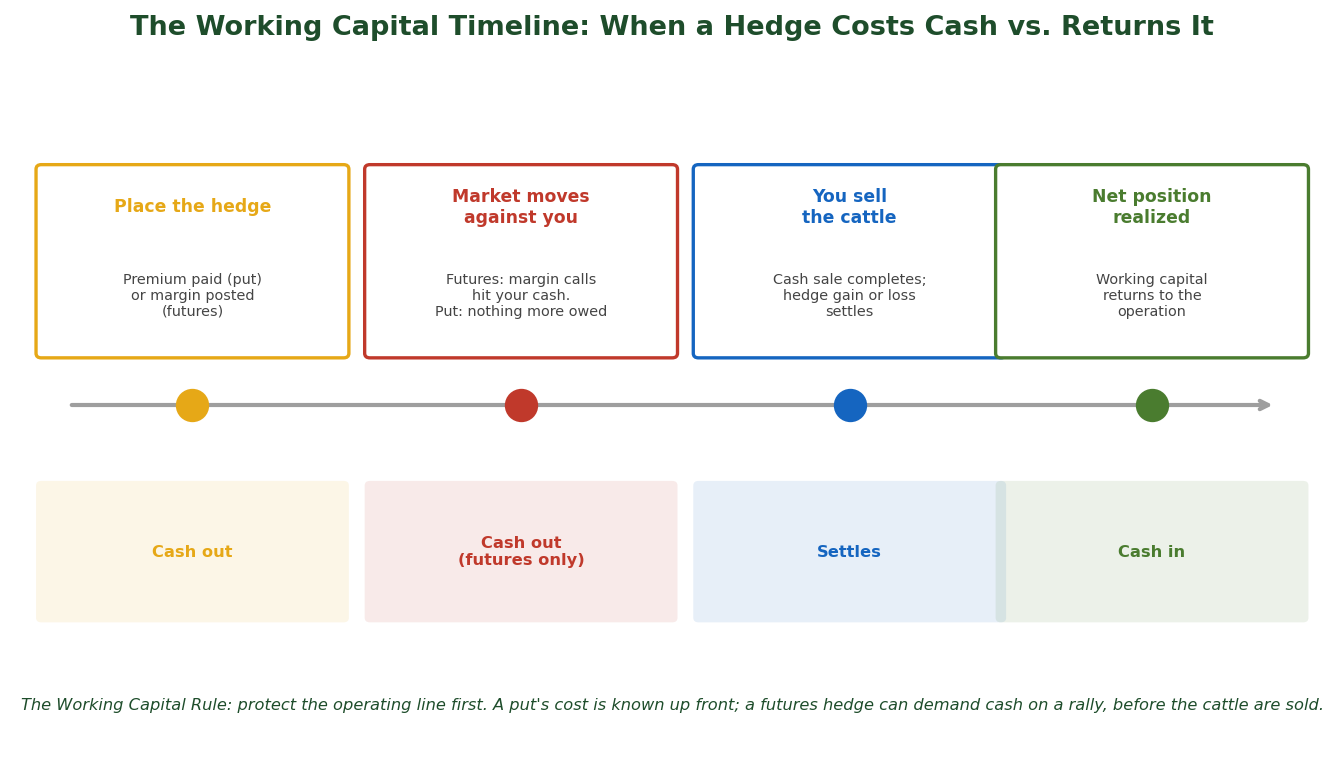

Here’s what we mean. When the board shows a profitable price for cattle you’ll sell in a few months, you have three real choices: lock it in with a futures hedge, set a floor with an option, or do nothing and take what the cash market gives you. Each one does something different to your cash position between now and the day those cattle leave the yard.

A futures hedge fixes your price, but if the market rallies before you sell, you owe variation margin — cash, today, on a position that’s “losing” on paper even though your cattle are worth more. We’ve watched more than one producer put on a textbook-correct short hedge, get hit with three margin calls during a summer rally, and swear off futures forever — not because the hedge was wrong, but because nobody planned for the cash flow. A bought option doesn’t do that. You pay the premium up front, and that’s the end of the cash demand, no matter which way the market runs.

Puts and Calls, in Plain Terms

A word on language, because it matters: options are not insurance. An option is an exchange-traded contract with a premium that’s fully at risk. Some producers also use Livestock Risk Protection (LRP), a USDA-subsidized insurance product that can set a floor, too — but LRP is sold by licensed crop insurance agents, not by brokers. If LRP fits your operation, your insurance agent is the right person to have that conversation with. This guide stays in our lane: the exchange-traded futures and options tools we work with as your broker.

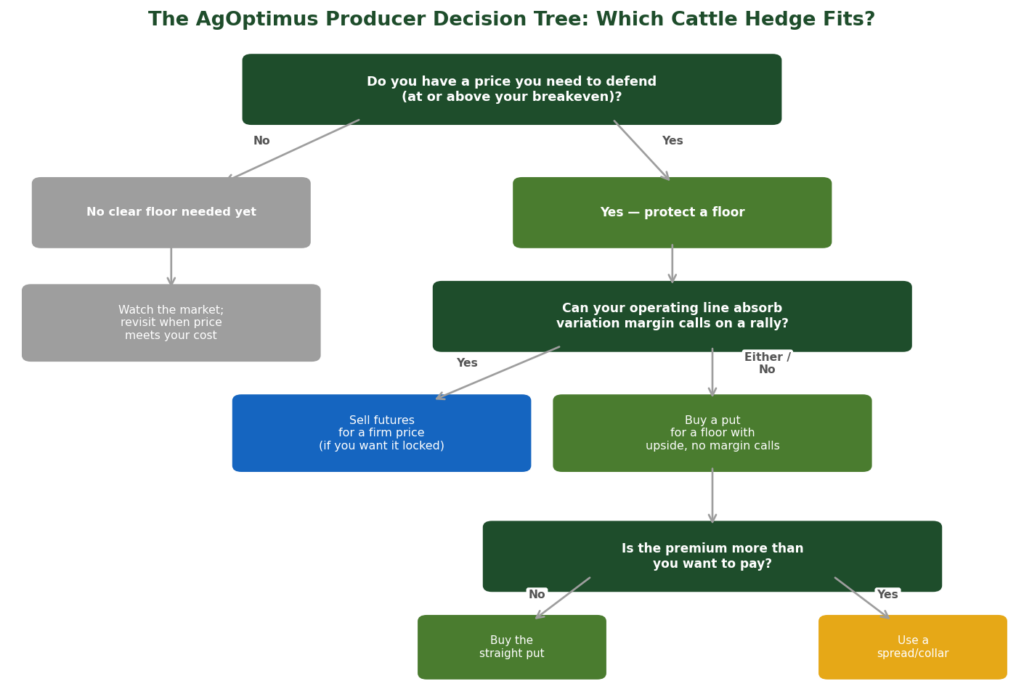

Should I Buy a Put or Sell Futures?

This is the question most producers are actually asking, so let’s answer it directly.

Sell futures when you want a firm, locked-in price and you have the operating line — and the temperament — to handle margin calls on a rally. Futures give you the tightest basis control and the most precise price, and for a feedlot managing large, predictable volume, that precision is worth a lot.

Buy a put when you want to protect a floor, but you either can’t stomach margin calls or you think the market might still run higher. You give up a little on the premium, but you keep your upside and never get a margin call. For most cow-calf operations and smaller backgrounders, that trade is worth making.

| Buy a Put | Sell Futures | |

|---|---|---|

| Sets a price floor | Yes | Yes (fixes the price) |

| Keeps upside if prices rise | Yes | No |

| Upfront cost | Premium (at risk) | Margin deposit |

| Margin calls possible | No | Yes |

| Maximum loss | The premium | Substantial; can exceed the deposit if unmanaged |

| Basis control | Good | Best |

| Best when | You want a floor and may want an upside | You want a firm locked price and can manage the margin |

A Worked Example: A 275-Head Cow-Calf Operation

The numbers land harder with a real operation in front of them, so here’s an illustrative one. (This is a composite example built to show the decision process — not a specific client.)

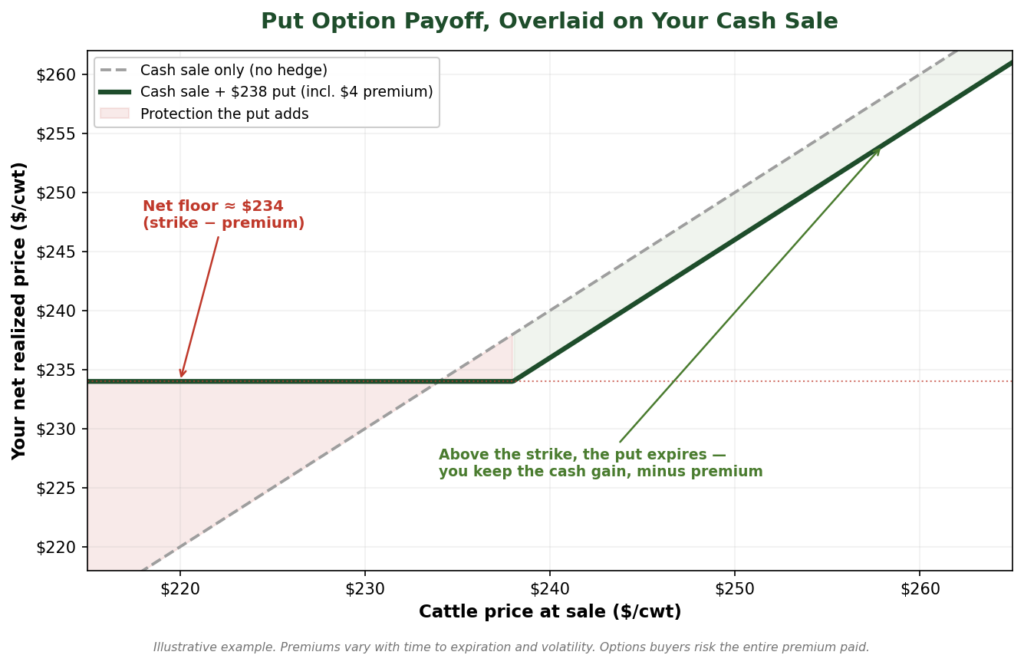

Illustrative composite. A 275-head Nebraska cow-calf operation expects to market roughly 250 head of calves in October, around 550 pounds each — about 137,500 pounds of production. Their cost of production pencils to a breakeven point they need to clear, and in late spring, the October feeder cattle board is trading at a level that would lock in a workable margin. They don’t want to sell the calves forward (weather and weight gain are still uncertain), and a string of margin calls over the summer would crowd their operating line right when they’re buying inputs.

The decision process: A feeder cattle contract is 50,000 pounds, so their 137,500 pounds is about 2.75 contracts — an odd lot. Selling 3 futures contracts would over-hedge them by about 12,500 pounds, and if the market rallied, they’d owe margin on cattle they don’t have and have to buy that excess back. Selling 2 would leave a third of their production unprotected. Instead, they buy 2 to 3 put options near the price they need to defend. The premium is a known cost that they can budget for. If feeder prices break by fall, the puts gain value and hold their floor. If prices rally, they let the puts expire, sell the calves at the stronger cash price, and their only cost is the premium.

The tradeoff: they paid a premium they won’t get back if the market simply holds steady. In exchange, they got a floor with no margin calls, the flexibility to size around an odd lot, and a number they could show their lender.

What this means for your operation: Your herd probably doesn’t divide evenly into contract sizes either. That’s not a problem to ignore — it’s a decision to make on purpose. Options give you a cleaner way to handle the odd remainder than an over-hedged futures position you’d have to buy back.

What this means for your operation: Your herd probably doesn’t divide evenly into contract sizes either. That’s not a problem to ignore — it’s a decision to make on purpose. Options give you a cleaner way to handle the odd remainder than an over-hedged futures position you’d have to buy back.How Do I Choose the Right Expiration? (And Why Weekly Options Exist)

An option only protects the window it covers. Buy one that expires in September for cattle you’ll sell in November, and you’ve spent premium on nothing. So the first rule of expiration is simple: the option has to be alive when your cattle actually move.

The second rule is subtler. CME lists weekly and serial Live Cattle options, not just the standard monthly contracts. These short-dated options exist for a reason most producers never use them for: hedging tightly around a known event — a Cattle on Feed report, a WASDE, a USDA number that could move the market — without paying for months of time value you don’t need. If your real risk is concentrated on a single reporting date, a weekly option can be a precise, lower-cost way to cover it.

Why Does the Same Put Cost More Some Weeks Than Others?

Because of volatility — and this is where timing quietly saves or costs producers real money.

An option’s premium is driven heavily by implied volatility: the market’s expectation of how much prices will move. When a disease headline hits, a report surprises, or funds shift, volatility jumps and premiums get richer overnight. The same put can cost meaningfully more the day after a shock than the day before.

The practical lesson we’ve watched play out for years: protection is cheapest to buy before the market gets nervous, not after. Producers who wait until the scary headline lands to set their floor almost always pay the price. The ones who hedge consistently — a little at a time, on a plan — tend to pay less for the same coverage over the long run, because they’re not buying protection at peak fear.

Contract Sizing and the Over-Cover vs. Under-Cover Decision

This is where the spec sheet meets the real world. A live cattle contract is 40,000 pounds; a feeder cattle contract is 50,000 pounds. Very few operations market in clean multiples of those weights, so nearly every hedge forces a choice: cover a little more than you have, or a little less.

Here’s the part that separates options from futures. If you over-cover with a short futures position and the market rallies, you owe variation margin on pounds you don’t actually own, and you have to buy that excess back — sometimes at a loss. If you over-cover with a bought put, the worst case on the extra coverage is the premium you paid for it. The risk is capped. That’s why options are friendlier to odd-lot herds: you can protect the bulk of your production and accept a small over- or under-cover on the remainder without taking on open-ended risk.

What Your Lender Will Ask Before Approving a Hedge Line

If you hedge through a brokerage account, especially with any size, your lender is part of this conversation whether you invite them or not. The cash that meets a margin call comes from somewhere, and that somewhere is usually the operating line the bank extended. The producers who get hedge programs approved smoothly are the ones who walk in already able to answer the banker’s questions.

In our experience, those questions come down to four:

- How much working capital does this tie up, and when? A banker wants to know the strategy’s cash demand, not just its logic. A put’s answer is clean: the premium, paid up front, and nothing more. A futures hedge’s answer is “it depends on the market,” which is exactly why the lender wants a plan for it.

- What’s your worst-case margin call? For a futures position, the bank will want a number: if the market moves hard against the hedge before you sell, how much cash could you be asked to post? This is where running margin scenarios ahead of time pays off — you walk in with the answer.

- How does this reduce risk overall? A bona fide hedge that offsets real cattle reduces the operation’s price risk; it’s not a speculative position that adds risk. Being able to show the cattle behind the hedge — and that the account is set up as a hedge account — is what makes that case.

- What happens if you have a short crop of cattle? If you forward-commit or over-hedge and then come up short on production, you may end up buying back a position. Lenders have seen it. Showing that you’ve sized conservatively against actual expected production answers the worry before it’s raised.

─── FOR FEEDERS AND EXPERIENCED HEDGERS ───

Everything above is what most producers need. What follows is for feeders, larger backgrounders, and operations already running hedge programs — the ones weighing premium against coverage against working capital, and answering the harder margin questions.

When Does an Option Spread Make Sense?

Once you’re buying protection regularly, the premium starts to bite, and a straight put can feel expensive. A spread is how experienced hedgers lower that cost — by giving up part of the protection or part of the upside in exchange for a smaller premium.

When to use one: a spread fits when you have a defined view of how far the market might move and you want defined-risk protection at a lower out-of-pocket cost. A feeder who wants a floor but doesn’t believe in a catastrophic crash might use a put spread to pay less for protection they expect to be “enough.” A producer comfortable capping upside in exchange for a cheap or free floor might use a collar. The tradeoff never changes: less premium, less open-ended benefit. You’re selling away part of the payoff to reduce costs.

Is It Safe to Sell Options to Collect Premium?

This is the question that separates a hedge from a hazard, so we’re going to be blunt about it.

Buying options has defined risk: the premium. Selling — writing — options is the opposite side of that trade, and it carries fundamentally different risk. It’s a legitimate tool in the right hands and a serious mistake in the wrong ones.

When it can make sense as a hedge: writing a covered call against cattle you already own is a legitimate commercial technique. You collect premium in a flat-to-mildly-higher market, accepting that you cap your upside above the call’s strike. Because you own the physical cattle, the “loss” above the strike is really upside you gave up — not an open-ended cash loss.

What Is a Hedge Account, and Why Does It Change My Margin and Limits?

This is the operational detail of generic content skips, and it’s exactly what your accountant and lender care about. The CFTC draws a real line between a bona fide hedger and a speculator, and which side of that line you’re on changes both your position limits and how your account is treated.

Two consequences follow, and both matter to a commercial operation. First, bona fide hedgers are exempt from the speculative position limits that constrain speculators — a producer hedging a genuine cash position can hold more contracts than a speculator’s cap allows, because the position offsets real physical exposure. Second, exchanges and FCMs treat hedge accounts differently from speculative accounts in their records, and hedge positions may carry different margin treatment than the same position held speculatively.

But none of that is automatic. To get hedge treatment, your account must be set up and designated as a hedge account with your FCM, and you must be able to show the cash-market position underlying it. That setup is a step a broker who knows the cattle business handles for you — and it’s one of the most common things producers don’t realize they’re leaving on the table.

How Does SPAN Margin Affect Cattle Hedging?

When you hold futures and options together — a hedge, a spread, a collar — your margin isn’t calculated leg by leg. CME uses a portfolio-based system (SPAN, now moving to SPAN 2) that looks at your overall position and nets offsetting risks.

The benefit is real: because SPAN recognizes that the legs of a hedge or spread offset, it can require far less margin than the gross of each position would suggest. A defined-risk spread, or an option held against a futures position, can be markedly more capital-efficient than the pieces priced separately. For a hedger managing working capital, that efficiency is worth understanding — and using.

The catch is just as real, and it’s where producers get caught: a SPAN margin number is not fixed. It’s a snapshot based on CME’s current risk parameters — the scan ranges and volatility inputs the exchange sets and updates regularly, especially around volatile periods and big reports. Your required margin on a written option or a spread can rise tomorrow without your position changing at all, simply because the exchange widened its parameters. And your FCM can require more than the exchange minimum.

This is the single most important thing to understand about margin if you’re selling options or running spreads: the margin you can comfortably carry today is not guaranteed to be the margin you’ll owe next week.

─── END OF ADVANCED SECTIONS ───

The Monday Morning Hedge Checklist

Before you place any cattle hedge, walk through this list. It’s the short version of everything above.

- Know your number. What price do you need to defend? Anchor it to breakeven, not hope.

- Check the operating line. Can you absorb margin calls, or do you need the defined cost of a put?

- Match the window. Does your protection cover the actual week or month your cattle move?

- Size to reality. Map your real marketing weight against the 40,000 / 50,000-pound contracts, and handle the odd lot on purpose.

- Mind volatility. Are you buying protection ahead of the risk, or paying up after the headline?

- Set the account up right. Is it a hedge account, with the cattle behind it documented?

- Stress the margin. Have you run the scenario for a hard move against you — before you place the trade?

How AgOptimus Helps Cattle Producers Use Options

- Start with your numbers. We begin with your cost of production, the cattle you need to cover, and your marketing window, so the strike, expiration, and tool actually fit your operation — not a template.

- Match the tool to the tier. A straight put, a spread to lower premium, or — for experienced operations — a hedged option-writing structure: we walk through the cost and the risk side by side, and we tell you when doing nothing is a legitimate answer.

- Set the account up right. We help make sure your account is established as a hedge account where appropriate, so your position limits and margin treatment reflect that you’re hedging real cattle.

- Simulate the margin and monitor it. We run margin scenarios before you commit and watch the position through expiration, so a SPAN parameter change or a volatility spike doesn’t catch you — or your lender — off guard.

Frequently Asked Questions

Should I buy a put or sell futures to hedge my cattle?

Buy a put when you want to protect a floor but keep your upside, or when you can’t comfortably absorb margin calls — your cost is the premium, with no margin calls. Sell futures when you want a firm, locked-in price and have the operating line to handle variation margin on a rally. Many operations use both: futures on cattle they want firmly priced, puts on cattle where they want a floor with upside.

Can cattle options eliminate margin calls?

Buying options eliminates margin calls — as an option buyer, your only cost is the premium paid up front, and you’ll never get a margin call on a bought option. This is a major reason producers who’ve been burned by variation margin on futures move toward puts. Note that selling (writing) options is different and does require margin.

Why do many producers prefer options over futures?

For most family cattle operations, a put is easier to maintain than a short futures hedge because it avoids variation margin calls that drain the operating line and preserves upside if the market rallies. Futures offer tighter basis control and a firm price, which larger feeders often want, but they demand cash at the worst possible moment — a rally — before the cattle are sold.

How do weekly cattle options work?

CME lists weekly and serial Live Cattle options alongside the standard monthly contracts. They let you hedge tightly around a specific event — like a Cattle on Feed report — without paying for months of time value. Because volatility tends to rise ahead of big reports, weekly options can be a precise, lower-time-cost way to cover a concentrated risk, though premiums still reflect that elevated volatility.

What is a hedge account, and why does it matter?

A hedge account is a brokerage account set up and represented as holding bona fide hedges — positions offsetting real or anticipated cattle, not speculative bets. It matters because bona fide hedgers are exempt from the speculative position limits that constrain speculators, and hedge accounts may receive different margin treatment than speculative accounts. To get that treatment, the account must be established as a hedge account with your FCM and you must be able to show the underlying cattle.

How does SPAN margin affect my cattle hedge?

CME calculates margin with a portfolio-based system (SPAN) that nets offsetting risks, so a hedge or spread can require far less margin than its legs would separately — a real capital-efficiency benefit. But SPAN figures aren’t fixed: the exchange updates its risk parameters regularly, especially around volatility, so your required margin can rise even when your position hasn’t changed. FCMs can also require more than the minimum. Run margin scenarios before committing.

Is selling options on cattle a good way to earn income?

Selling options is not a beginner’s income strategy. Writing a covered call against cattle you own is a legitimate hedge that caps your upside in exchange for premium. But selling a naked option — one not backed by physical cattle or an offsetting position — exposes you to large, potentially open-ended losses and ongoing margin demands. It should only be done with a full understanding of the risk and a broker who sizes it to your operation.

How do cattle options affect my working capital and my lender?

A bought option’s cost is known up front — the premium — which makes its working-capital impact easy to plan and easy to explain to a lender. A futures hedge can demand variation margin on a rally, before the cattle are sold, which is why lenders want a worst-case margin number and a plan for it. Setting up the account as a bona fide hedge account also helps demonstrate to the bank that the position reduces risk rather than adds it.

Educational Disclaimer: This material is for educational purposes only and is not individualized trading, investment, or risk-management advice. Trading futures and options involves substantial risk of loss and is not suitable for all investors. Options buyers risk the entire premium paid. Selling options can involve substantial and potentially unlimited risk. The case study and examples here are hypothetical illustrations and do not represent any specific client or guarantee any result. Margin requirements are set by the exchange and your FCM and can change. Past performance is not necessarily indicative of future results. AgOptimus is a registered DBA of Optimus Futures LLC [NFA ID 0481133]. Each producer should evaluate any strategy against their own financial condition and risk tolerance.