By Nathan Harris · Corn producer and cattle feeder, and a registered broker with Ag Optimus

Check the corn futures price on your phone, then call your local elevator for a cash bid. The two numbers won’t match. That difference, called the basis, is the gap between the futures price on the board and the cash price you’re offered. The board price doesn’t tell you what your corn will fetch at your elevator — basis does. It is one of the most important numbers in corn marketing, and one that many growers overlook.

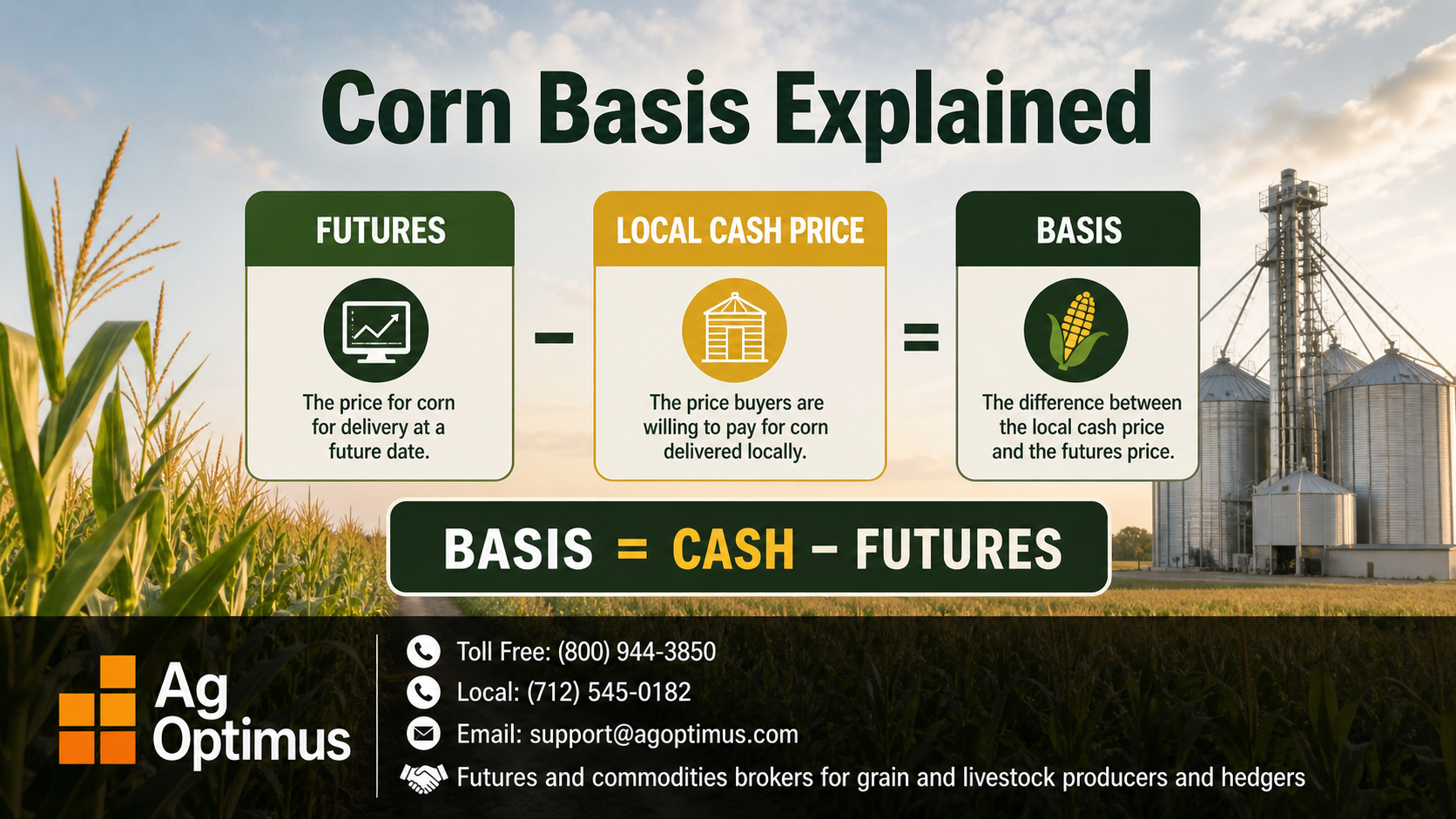

What Corn Basis Actually Is

Basis is a simple subtraction: your local cash price minus the relevant futures price. If the December corn futures contract is trading at $4.30 and your elevator is bidding $4.05 for cash corn, your basis is 25 cents under — written as “−25” or “25 under.” If the elevator were bidding $4.40 against that same board, your basis would be 10 cents over, or “+10.”

That single number captures the local factors the national futures market does not: distance to end users, local transportation costs, nearby demand, and storage capacity. The futures board reflects the corn market as a whole. Basis reflects your corner of it.

Strong versus weak basis, in plain terms. A stronger basis means the cash price is at or above the futures price, because local buyers are competing for corn. A weaker basis means the cash price sits well below futures, usually because corn is plentiful locally or expensive to move. A move from −30 to −15 strengthens the basis by 15 cents, which increases your cash return regardless of futures price changes.

Why the Cash Price and the Futures Price Differ

The futures price is a single national reference price established on the exchange. The cash price at your elevator is a local, physical price for real corn that has to be moved, stored, and used. Several primary factors contribute to the disparity between cash and futures prices.

Transportation and logistics are the primary factors. Corn grown far from a processor, river terminal, or feed market costs more to move, and that expense is deducted from the local bid price. The wider freight system becomes apparent here too: when the Mississippi or Ohio runs low and barge freight jumps, interior basis often weakens because it costs more to float corn to the Gulf. When export demand picks up at the Gulf or Pacific Northwest, river-terminal basis can firm as those buyers draw bushels. Rail availability operates under similar principles. A farm near steady local demand usually sees a stronger basis than one farther out, even in the same state.

Local supply and demand matter just as much. An area containing many ethanol plants, feedlots, or export terminals competing for corn has a firmer basis. An area that grows a lot of corn with few local buyers is likely to have a weaker basis, because the grain has to travel to find a home.

Storage and timing round it out. When all of you are harvesting at the same time, and bins and elevators fill up, basis usually weakens, because there is more corn than the local market can handle right there, right then. As that corn gets used through winter and spring, basis often strengthens.

The Mistake I Watch Growers Make Every Fall

From a broker’s perspective, the most common basis mistake is treating the futures price as if it were the whole story. A grower sees the board rally, feels good about it, and hauls corn to town at harvest, right when local basis is weakest. The board looked strong, but the cash bid was weaker than the board suggested, because the basis quietly eroded the cash price.

Conversely, two elevators twenty miles apart can post noticeably different cash bids on the same day, because their local demand, storage space, and freight situations differ. A grower who focuses on a single bid or only watches the board misses the picture. Basis is local, and it pays to know yours.

Why Basis Is a Separate Decision From the Board

Here is the part that changes how a grower markets corn: the board price and the basis can be set at different times. They do not have to move together, and often they don’t.

Short futures hedges or hedge-to-arrive contracts let growers secure futures prices when the board looks attractive. They keep the basis open so it can be set later when local conditions improve. The reverse happens too: local basis may strengthen even when the board is weak, which can be a good moment to set basis or move physical corn while waiting for the board to move.

Making separate board and basis decisions usually leads to better cash prices than lumping everything into a single “sell or don’t sell” choice. A strong board price can be undercut by a weak basis. A strong basis can improve a weak board. Watching both and acting on each when it looks favorable is the essence of disciplined corn marketing.

How to Read Basis in a Market Update

Once you understand that basis functions as an independent market lever, you’ll better grasp market recaps you already read. When a morning or afternoon cash-grain update says corn basis was “steady to stronger” or “flat to lower,” it is describing basis moving against futures, not the futures price itself. You will see lines like basis strengthening at a river terminal while weakening at an interior processor, or a plant dropping its bid a few cents ahead of expected farmer selling.

Those small moves matter even on a quiet day for futures. A farmer’s cash price equals futures plus basis, so the board can sit still while basis firms a nickel and lifts your local bid, or the board can rally while basis weakens enough to eat up most of the gain. Reading both numbers and comparing today’s basis to what is normal for your area this time of year tells more than watching the board alone. University extension services and cash-bid maps publish local basis and historical averages, which help make that comparison easier.

Sell Off the Combine, or Store and Wait for Basis?

This is the basis question that comes up most in farm meetings and around the coffee table: sell corn off the combine at harvest, or store it and wait for basis to improve? There is no one correct answer, but basis is at the center of it. Harvest-time selling brings the weakest basis of the year. Storage bets that basis gains and carry cover holding costs.

I see two repeated mistakes. The first is not selling when the basis is strong — growers pass on a strong local bid because the board appears likely to go higher. The second is the opposite: leaving grain in the bin too long, hoping basis will keep climbing, until quality slips or the seasonal window closes. Storing corn is a marketing decision with its own costs, and it deserves a target: a basis level or a date to act on.

How Basis Behaves Through the Year

Basis tends to follow a seasonal rhythm, though every year and every location is different. A common pattern looks like this:

-

- Harvest: basis is weakest at harvest, as a flood of corn hits full bins and elevators at once.

-

- Winter: as harvest pressure clears and corn moves into use, basis starts to firm.

-

- Spring and summer: with old-crop supplies tightening before the next harvest, basis reaches its strongest, especially where local demand is steady.

Every year and region is unique, so treat this as a general tendency rather than a rule. Local plant shutdowns, transportation disruptions, local crop size, and river conditions can all push basis off its usual path. Tracking your own elevator’s basis over a few years teaches more about your local pattern than any general rule can.

Putting Basis to Work in a Marketing Plan

Knowing basis is useful only if it informs decisions. A few practical habits help.

Document your local basis the way you track the board, so you can determine whether today’s bid matches the typical strength for this period. Seek bids from multiple buyers when you can, since basis varies by location. When the board looks attractive but basis is weak, use a deferred-basis contract, a forward or futures order, or options — for example, sell futures now and set the basis later. And when basis is strong, recognize that as its own opportunity, even if the board isn’t at its best.

One piece of practical wisdom growers share is worth repeating: watch the nearby local ethanol plants or feedlots and the river traffic, not just the board. If a nearby plant is hungry for corn, or barge demand is pulling hard at the river, the basis can firm regardless of what futures are doing. The board reflects the whole country. The basis reflects the local processing facility down the road.

None of this requires predicting the market. Manage basis as an independent decision, not an afterthought to futures.

A Note for Mixed Crop–Cattle Operations

For an operation that both grows and feeds corn, basis cuts two ways. A weak local basis that frustrates a corn seller is, from the feeding side, cheaper feed in the bunk. An operation that produces and consumes its own corn effectively captures the local basis when it feeds the crop instead of selling it. Separate the decision to sell from the decision to feed, then measure each against local basis levels.

The Bottom Line on Corn Basis

The futures board tells you what corn is worth nationally. Basis tells you what it is worth at your local elevator, on your road, in your season. Growers who market corn well watch both numbers, know the two can be set separately, and treat a weak basis as a reason to wait or reach for a tool. A weak basis at the scale should always be expected, never a surprise.

Reading local basis well requires experience that develops over time, and it is exactly the kind of thing a broker who works with producers in your region can help with. The team at Ag Optimus works with corn growers and mixed crop–cattle operations on reading basis and fitting it into a marketing plan.

This is educational content for general purposes from Ag Optimus, a registered DBA of Optimus Futures LLC, an NFA-member and CFTC-registered Introducing Broker [NFA ID 0481133]. It does not provide personalized trading or risk-management guidance, and it is not a recommendation or solicitation to trade futures or options. Trading futures and options carries a significant risk of loss and is not suitable for all investors, and historic performance doesn’t guarantee future results. Each operation is different. Assess strategies based on your production costs, marketing plan, financial situation, and risk tolerance. Consult your broker before deciding.

Frequently Asked Questions

What is corn basis?

Corn basis is the difference between your local cash price and the relevant corn futures price: cash price minus futures price. If December futures are at $4.30 and your elevator bids $4.05, you are 25 cents under. Basis reflects local factors like transportation, nearby demand, and storage that the national futures price does not.

Why is the cash price at my elevator different from the futures price?

The futures price is a national benchmark; your elevator bid reflects local supply and demand, transportation, and storage costs, so cash bids rarely match the board. That is why the price you are offered locally is almost never the same as the number on the screen.

When is corn basis usually strongest?

Corn basis is usually weakest at harvest, when a flood of corn fills bins and elevators at once, and tends to strengthen through winter and into spring and summer as supplies tighten before the next harvest. Treat that as a general pattern, not a rule — local disruptors like plant closures or transport problems can change it.

Can I set the futures price and the basis at different times?

Yes. Use a short futures hedge or a hedge-to-arrive contract to lock the futures price, and leave the basis to be set later when local conditions improve. Treating the board and basis as separate decisions often produces a better final cash price.

Does the basis matter if I feed my own corn to cattle?

Yes — a weak local basis lowers your feed cost, so feeding corn instead of selling it effectively captures that basis. Operations that both grow and feed corn benefit from treating the corn they sell and the corn they feed as separate decisions, each measured against local basis.