How to Build a Margin Management Policy for Your Cattle Operation

Most producers manage price risk one decision at a time. A good price shows up, they sell some cattle; a scary headline hits, they think about a hedge; the rest they carry and hope. That works until the year it doesn’t — the year the market hands back the margin before they acted, or the year fear pushed them to lock in at the wrong time. A margin management policy replaces that one-decision-at-a-time habit with a written plan: you know your cost of production, you know the margin you need, and you decide ahead of time how you’ll act when the market offers it. It’s how the most disciplined cattle operations run the risk side of the business like a business.

This guide is written for cattle producers — including first-time hedgers — and the lenders who want to see risk managed on purpose, not by gut feel. The goal throughout is to manage price risk, not to guarantee a margin, which no tool can do.

Key Takeaways

Key Takeaways

- A margin management policy is a written plan for protecting the difference between your revenue and your cost of production, not a single trade, and not a promise of profit.

- It starts with your breakeven. You can’t manage a margin you haven’t calculated, so cost of production comes first.

- The futures market is a planning tool, not just a trading venue. Deferred contract prices let you see your projected margin months ahead and decide whether it’s worth acting on.

- A policy removes emotion. Deciding your rules in calm markets keeps you from reacting badly in volatile ones.

- It scales to any operation. Whether you market 50 head or 5,000, the breakeven-first discipline is the same.

- Your lender will respect it. A written risk policy tells a banker the operation is managed deliberately, which matters when they’re extending your operating line.

What Is a Margin Management Policy?

A margin management policy is a written set of rules for how your operation protects its margin — the gap between what you expect to bring in and what it costs to produce. It answers four questions in advance: what margin do I need, how will I know when the market is offering it, what tools will I use, and how will I keep records.

The point isn’t to predict the market. It’s to make the decisions you’d otherwise face under pressure — prices spiking or crashing, your stomach involved — ahead of time, on paper, when you can think clearly. Marketing by feel tends to make you boldest when you should be cautious and most cautious when you should be bold; a written policy keeps you steady, keeps you consistent, and gives you a record you can show your lender. A policy doesn’t tell you the market will go your way. It tells you what you’ll do either way.

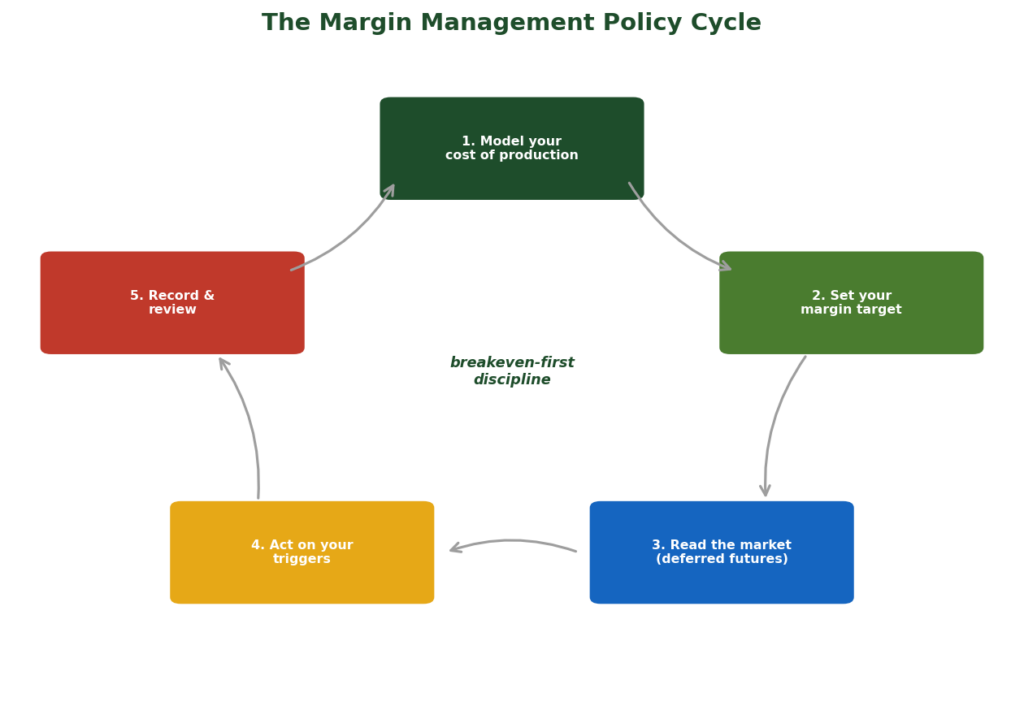

The Building Blocks of a Margin Management Policy

A workable policy has five parts. None of them requires you to predict prices.

Cost of production. Everything starts here, per the AgOptimus Breakeven-First Rule above. For a cattle feeder, that’s the feeder calf, the feed, and the rest — vet, labor, interest, yardage. For a cow-calf producer, it’s the cost to get a calf to its marketing weight. This is your breakeven.

Cost of production. Everything starts here, per the AgOptimus Breakeven-First Rule above. For a cattle feeder, that’s the feeder calf, the feed, and the rest — vet, labor, interest, yardage. For a cow-calf producer, it’s the cost to get a calf to its marketing weight. This is your breakeven.- Your margin target. The margin you need to clear, above breakeven, to keep the operation healthy. Not the home-run price — the price that works.

- Price discovery. Use the futures market to see your projected margin months out. Deferred contracts show you what the market is currently offering for the months you’ll market in, so you can judge whether the margin on the table is good or poor.

- Your tools and triggers. Decide in advance which tools you’ll use and when: use a put to set a floor, a futures hedge to lock a price, or a spread to lower the premium, and the conditions that would prompt each. In later guides, we’ll walk through how those tools, your inventory, and your FCM’s margin policies fit together.

- Records and review. Write down what you did, when, and why, and review each season. That’s what turns a one-time decision into a repeatable discipline.

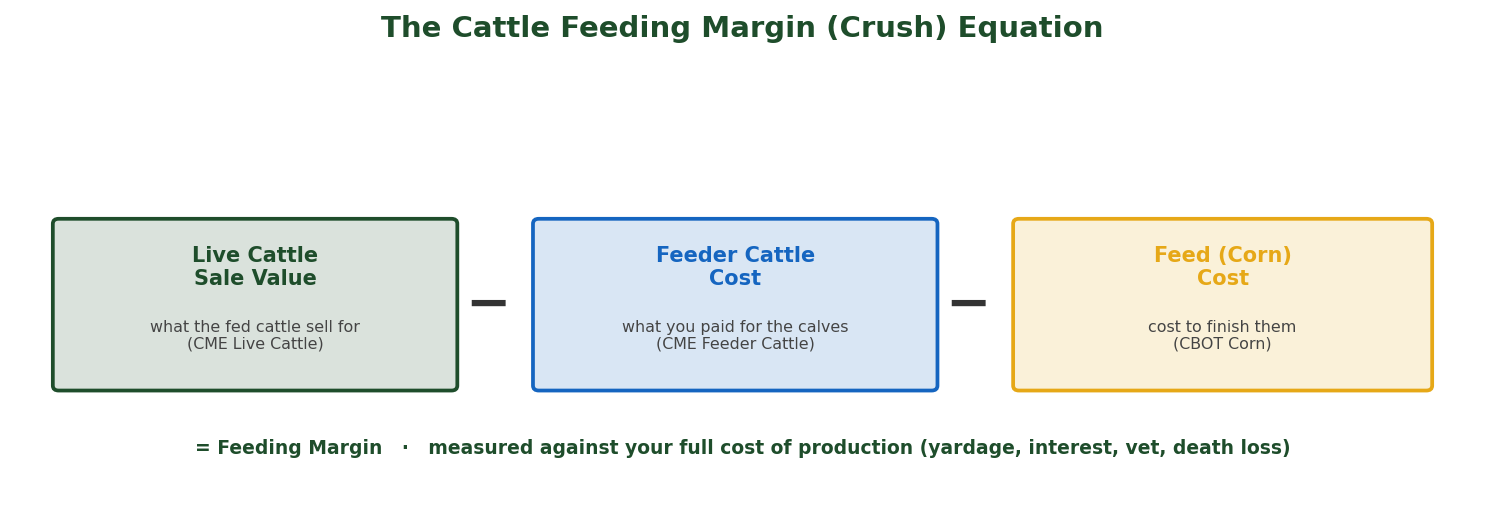

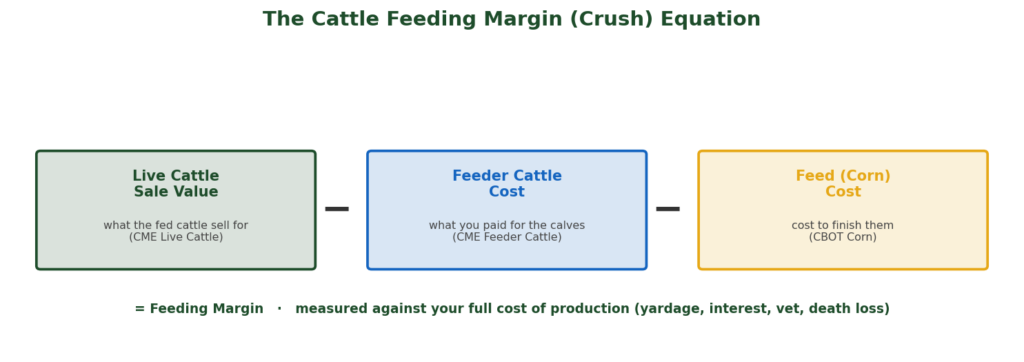

The Cattle Feeding Margin: A Worked Example

Here’s where the idea gets concrete. A feeder’s margin is built from the three futures markets in the crush formula above — live cattle, feeder cattle, and corn — and the futures market lets you estimate that margin before you even place the cattle.

The Discipline That Protects You: Hedging Is Not Speculating

There’s one rule that sits above all the others, and extension economists have repeated it for decades: keep hedging and speculating separate. A hedge offsets the price risk of real cattle you own or will produce; speculation is taking a market position to bet on price, with no physical production behind it. They are different activities, and a margin management policy is built entirely on the first.

This matters in practice. A bona fide hedge — one tied to real or anticipated cattle — is risk management, and it’s treated that way, including in how your account is set up. The moment a position stops tracking your production and becomes a bet on the market, you’ve left hedging and entered speculation, which carries a different risk entirely.

Where LGM Insurance Fits

Here’s the useful part for a beginner: LGM is built on the very same crush — Live Cattle minus Feeder Cattle minus Corn — just wrapped in an insurance policy with no margin calls. It’s sold by licensed crop insurance agents, not brokers, so an agent is the right person for it. Coverage terms, availability windows, and subsidy levels are set by USDA and can change, so your crop insurance agent is the right source for current details. Futures and options are the flexible alternative we handle directly, and the two can work side by side. The policy is the plan; LGM, futures, and options are tools that serve it.

How AgOptimus Helps You Build and Run Your Policy

- Start with your breakeven. We help you model your cost of production and projected revenue, so your policy is anchored to a real number, not a guess.

- Show you the margin the market is offering. We use deferred futures to put your projected margin in front of you for the months you’ll market in, and help you judge it against where it’s been.

- Match the tools to your rules. When your policy calls for action, we walk through which tools — futures, puts, spreads — fit the situation, side by side with the costs and risks.

- Keep it disciplined and on record. We help you execute the decisions you direct, keep the records your lender will want, and review the policy each season. Clean records and a written policy make it easier to explain your risk plan to your banker and justify your operating line. Your account, your decisions; our guidance and execution.

Frequently Asked Questions

What is a margin management policy?

A margin management policy is a written plan for protecting the margin between your expected revenue and your cost of production. It defines, in advance, the margin you need, how you’ll use the futures market to see what the market is offering, which tools you’ll use to act, and how you’ll keep records. It’s a discipline for managing price risk deliberately rather than reacting to the market one decision at a time. It does not guarantee a margin — no tool can — but it manages the risk to it.

How do I calculate my breakeven for cattle?

Your breakeven is your full cost of production expressed as a price. For a cattle feeder, that means adding the feeder calf cost, feed, yardage, interest, vet, labor, and expected death loss, then dividing by the expected sale weight to get a breakeven per hundredweight. For a cow-calf producer, it’s the cost to bring a calf to marketing weight. Everything in your margin policy is measured against this number, so it must be accurate and complete.

What is the cattle crush or feeding margin?

The feeding margin, often called the crush, is live cattle sale revenue minus the cost of the feeder cattle minus the cost of the corn to feed them: Live Cattle − Feeder Cattle − Corn. Because all three have actively traded futures contracts, a feeder can use deferred futures prices to estimate the projected margin on cattle before they’re even placed, which is what makes margin planning possible.

What is LGM insurance for cattle?

Livestock Gross Margin (LGM) insurance is a USDA-subsidized insurance product that protects against a decline in the cattle feeding margin, bundling the fed-cattle price and the feeder and corn input costs into a single policy. It’s built on the same crush formula, and it’s sold by licensed crop insurance agents, not brokers. It can complement a futures-and-options margin policy; a licensed agent is the right person to size and sell it.

How do I know if a margin is good enough to protect?

The simplest rule is to measure it against your breakeven: protect a margin that clears your full cost of production by a comfortable cushion, and lean in harder when the margin is unusually strong. You don’t need a complicated model to start — knowing your breakeven and acting when the market clears it with room to spare puts you ahead of most operations.

Is a margin management policy only for large operations?

No. The framework scales to any size — the building blocks are the same whether you market 50 head or 5,000. Smaller operations may use fewer contracts or different tools, but the discipline of knowing your breakeven, setting a margin target, and deciding your rules in advance is just as valuable, arguably more so, when every dollar of margin counts.

How is hedging different from speculating?

A hedge offsets the price risk of real production — cattle you own or expect to produce. Speculation is a market position taken to profit from price moves, with no physical production behind it. A margin management policy is built entirely on hedging; every position should trace back to actual or anticipated production. Keeping the two separate is the oldest discipline in risk management, and the most important.

Educational Disclaimer: This material is for educational purposes only and is not individualized trading, investment, or risk-management advice. Trading futures and options involves substantial risk of loss and is not suitable for all investors. A margin management policy helps manage price risk but does not guarantee any margin, profit, or outcome. Options buyers risk the entire premium paid; selling options can involve substantial and potentially unlimited risk. The examples here are hypothetical illustrations and do not represent any specific client or guarantee any result. Margin requirements are set by the exchange and your FCM and can change. Past performance is not necessarily indicative of future results. AgOptimus is a registered DBA of Optimus Futures LLC [NFA ID 0481133]. Each producer should evaluate any strategy against their own financial condition and risk tolerance.