Introduction

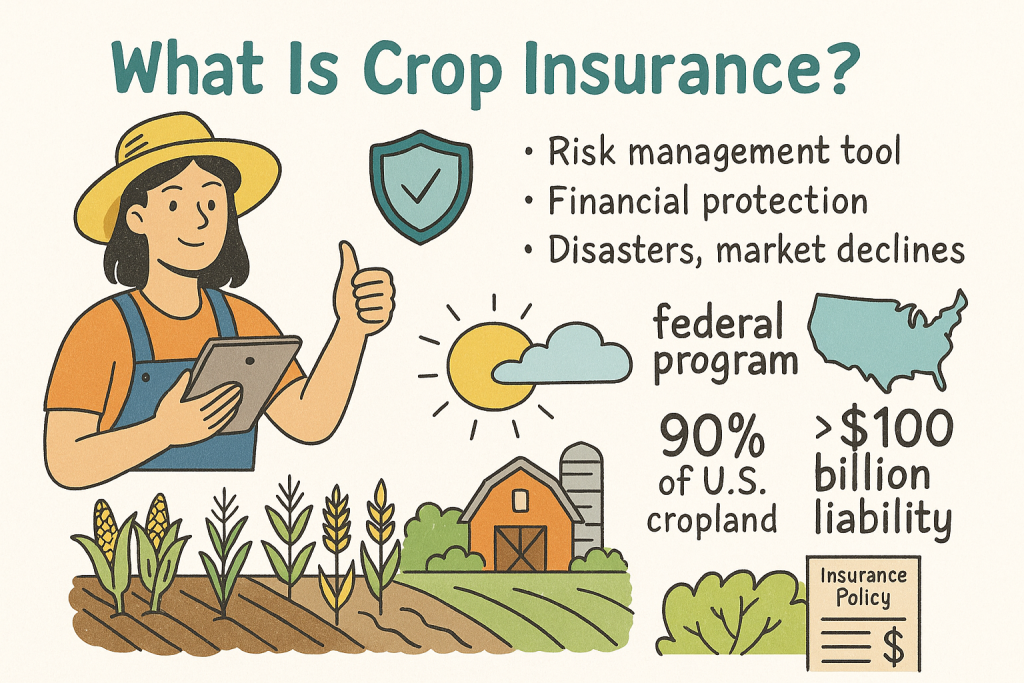

Crop insurance is a federally subsidized risk management tool that protects agricultural producers against financial losses from natural disasters, disease, and market price declines. As a cornerstone of the nation’s farm safety net, crop insurance programs are specifically designed to support the stability and sustainability of U.S. agriculture. The federal crop insurance program covers approximately 380 million acres of U.S. farmland, representing nearly 90% of the country’s cropland, with total insured liability exceeding $100 billion annually.

This comprehensive insurance coverage serves as a critical component of America’s farm safety net, protecting both individual farmers and the broader food system from catastrophic agricultural losses.

What This Guide Covers

This guide explains the federal crop insurance program structure, types of coverage available through approved insurance providers, how premium subsidies work, and practical steps for obtaining protection. We do not cover international programs or non-agricultural insurance products.

Who This Is For

This guide is designed for farmers, ranchers, and agricultural producers considering crop insurance options. Whether you’re a beginning farmer exploring risk management tools or an experienced producer evaluating coverage levels, you’ll find practical information about federal and private insurance programs.

Why This Matters

Crop insurance protects more than $192 billion in agricultural production value, ensuring farm business continuity in the face of natural disasters. Without adequate coverage, a single weather event can devastate years of farm income, threatening both individual operations and national food security.

What You’ll Learn:

- Core definition and purpose of crop insurance protection

- Main types of coverage include multiple-peril crop insurance and crop hail insurance

- Federal program structure involving the Risk Management Agency and the Federal Crop Insurance Corporation

- Practical steps for evaluating and obtaining appropriate insurance coverage

Understanding Crop Insurance Fundamentals

Crop insurance is a financial protection system that transfers agricultural production risks from farmers to insurance companies through formal policies backed by federal government support.

This risk management approach allows agricultural producers to protect against yield losses and revenue declines that could otherwise threaten the viability of their farms. The system operates through a public-private partnership where private insurance companies sell and service crop insurance policies under federal oversight and substantial premium subsidies.

The federal crop insurance program covers natural disasters, including drought, hail, frost, flooding, disease, and pest damage that reduce crop yields or quality below normal levels.

Definition and Core Purpose

Crop insurance protects agricultural producers against crop loss from natural disasters or revenue loss from price declines. This dual protection ensures farmers can maintain business operations even when facing either production shortfalls or unfavorable commodity prices during harvest.

The program serves as a cornerstone of agricultural risk management, providing stability that enables long-term farm planning and investment decisions. This protection connects directly to the broader farm safety net programs that Congress passed beginning in the 1930s, following devastating crop losses during the Great Depression.

Commodities Covered by Crop Insurance

Federal crop insurance covers a wide range of commodities, including major row crops such as corn, soybeans, wheat, cotton, rice, barley, oats, and sorghum. Specialty crops like peanuts, potatoes, and certain fruits and vegetables are also eligible for coverage under specific policies. In total, the program provides insurance coverage for over 120 agricultural commodities, ensuring broad access for diverse farming operations across the United States.

Federal vs Private Insurance Programs

The distinction between federally subsidized programs and private crop insurance lies in government oversight and premium support. The Federal Crop Insurance Corporation oversees the federal program through the Risk Management Agency, which regulates approved insurance providers that sell standardized policies with premium subsidies.

Private insurers also offer crop hail insurance and specialty coverage outside the federal program, regulated by state insurance departments rather than federal oversight. Building on this federal foundation, private insurance companies provide supplemental protection that farmers can purchase to address specific risks not covered by federal policies.

Alternative Risk Management Tools: CME Futures and Options

In addition to crop insurance, agricultural producers may consider using financial instruments, such as CME (Chicago Mercantile Exchange) futures and options contracts, as alternatives or complements to traditional crop insurance. These market-based tools allow farmers to hedge against price volatility by locking in prices or purchasing options to protect against adverse price movements.

While CME futures and options do not cover physical crop losses from natural disasters, they serve as effective tools for managing revenue risk from fluctuating commodity prices. Utilizing these instruments requires market knowledge and active management, but can be a valuable part of a diversified risk management strategy.

Transition: Understanding these fundamental concepts provides the foundation for exploring the specific types of coverage available to agricultural producers.

Types of Crop Insurance Coverage

Agricultural producers can choose from several insurance coverage options based on their specific crop production risks and financial protection needs. As a key federal support program, the federal crop insurance program serves as a cornerstone of risk management for U.S. farmers, providing vital protection against a range of agricultural risks.

Each coverage type addresses different aspects of farm risk management, from basic catastrophic protection to comprehensive revenue guarantees. For example, yield-based crop insurance protects against losses from reduced yields due to natural disasters, while revenue-based policies cover declines in both yield and market price, offering broader financial security.

Multiple Peril Crop Insurance (MPCI)

Multiple-peril crop insurance is the cornerstone of the federal crop insurance program, providing protection against multiple natural disasters through standardized policies. This federally subsidized coverage protects over 120 agricultural commodities, with participation in major U.S. crops reaching 89% in 2024. Among the various perils covered, drought and high temperatures are the leading causes of indemnified losses in the federal crop insurance program.

MPCI policies must be purchased before planting deadlines, with coverage levels ranging from Catastrophic (CAT) coverage at 50% loss threshold to higher protection levels up to 85% of normal yields. The program requires farmers to insure all eligible acreage of covered crops in each county, preventing adverse selection that could undermine actuarial soundness.

Farmers pay administrative fees of $655 per crop per county for CAT coverage, or $30 plus premiums for higher coverage levels, with the federal government providing substantial premium subsidies.

Crop-Hail Insurance

Crop hail insurance provides private insurance coverage focused specifically on hail and fire damage, operating independently from federal programs under state insurance department regulation. This coverage offers flexibility that many farmers value, including the ability to purchase protection year-round during the growing season and after planting when weather risks become more apparent.

Unlike federal programs, crop hail insurance typically features lower deductibles and can supplement MPCI coverage for comprehensive protection. Private insurers design these policies to address the localized nature of hail damage, which can devastate individual fields while leaving neighboring farms unaffected.

Revenue Protection Insurance

Revenue protection represents the most popular form of crop insurance, accounting for the majority of total insured liability in the federal program. As a form of crop revenue insurance, this coverage protects farmers against revenue losses caused by low yields or declining crop prices, ensuring that total farm revenue does not fall below guaranteed levels.

The insurance calculates protection based on expected revenue using spring planting-time prices compared to actual harvest revenue, incorporating both yield performance and commodity price data. This approach provides more comprehensive financial protection than yield-only coverage, recognizing that farmers face both production and marketing risks.

Key Points:

- MPCI covers 120+ crops with mandatory participation for all eligible acreage

- Crop hail insurance offers flexible, supplemental protection from private insurers

- Revenue protection, as a type of crop revenue insurance, addresses both yield and price risks affecting farm income

Transition: These coverage options operate within the broader federal program structure that determines eligibility, pricing, and administrative procedures.

How the Federal Crop Insurance Program Works

The federal crop insurance program operates through a complex public-private partnership, with total program costs in 2024 of approximately $12.37 billion, including premium subsidies, administrative costs, and other expenses. Administrative costs are incurred in the management and delivery of the program, with contributions from both the government and private sector. The U.S. Department of Agriculture (USDA), as the relevant department, oversees the federal crop insurance program, ensuring program integrity and actuarial soundness. Payments are also made to approved insurance providers and farmers as part of the program’s financial structure, balancing private-sector efficiency in policy sales and claims adjustment with federal oversight.

Risk Management Agency and FCIC Role

The Risk Management Agency provides program oversight and supervision of approved insurance providers that sell and service federal crop insurance policies nationwide. The Federal Crop Insurance Corporation board approves new insurance products through the 508(h) submission process, ensuring all coverage options meet federal standards for actuarial soundness and farmer protection.

Standard Reinsurance Agreements between the federal government and private insurance companies define the terms under which insurers participate in the program, including reinsurance coverage that protects companies against catastrophic losses. The program maintained a 0.86 loss ratio in 2023, indicating that indemnity payments represented 86% of total premiums collected.

Premium Subsidies and Cost Sharing

The federal government provides premium subsidies that significantly reduce farmers’ costs, with CAT coverage receiving full subsidies, while higher coverage levels receive decreasing government support. Administrative and operating expenses are shared between farmers and the federal government, with farmers paying administrative fees and the government covering most operating expenses for private insurance companies.

This subsidy structure encourages widespread participation while maintaining cost control, as farmers face higher premiums when selecting the maximum coverage level. The government’s large share of total program costs reflects the policy priority of maintaining agricultural production stability and food security.

Coverage Levels and Unit Types

Farmers can choose from five insured unit types: basic, optional, enterprise, multicounty enterprise, and whole-farm units, with each affecting premium costs and indemnity payments differently. Different types of land, such as owned or rented land, are categorized and insured as separate units within crop insurance programs, allowing coverage to be tailored to each parcel. Coverage level selection determines the percentage of crop value that receives insurance protection and establishes deductible thresholds that farmers must meet before receiving indemnity payments.

The program offers both farm-level and county-level average yield and revenue options, allowing producers to select protection based on either their individual production history or broader county performance data. All participants must follow good farming practices and meet conservation compliance requirements to protect wetlands and highly erodible lands and maintain eligibility.

Transition: While the federal program provides comprehensive coverage, farmers often encounter specific challenges when navigating insurance decisions.

Common Challenges and Solutions

Agricultural producers frequently face complex decisions when evaluating crop insurance options, particularly regarding coverage limitations and compliance requirements that affect policy effectiveness. Prior to recent legislative changes, many of these challenges were more pronounced, with historical loss ratios and earlier regulations limiting both the structure and participation in crop insurance programs.

Understanding Coverage Limitations

Solution: Review the specific perils covered and excluded in policy documents, paying particular attention to situations such as the inability to market crops without physical damage or disease, and to pest control requirements that must be met for coverage.

Many farmers discover too late that certain types of losses are not covered under standard policies, underscoring the importance of working with experienced insurance agents to understand policy terms.

Choosing the Right Insurance Type

Solution: Evaluate farm-specific risks, crop types, and financial goals with insurance specialists who understand both federal programs and private insurance options available in your area.

Consider combining multiple-peril crop insurance with crop hail insurance for comprehensive protection, as this approach addresses both broad natural disaster risks and localized weather events.

Meeting Compliance Requirements

Solution: Understand conservation compliance rules that protect wetlands and highly erodible lands, as violations can result in loss of eligibility for all federal farm programs, including crop insurance.

Stay current with farm bill updates affecting cover crops and prevented planting provisions, which can impact both coverage options and payment calculations.

Transition: Understanding these challenges prepares producers to make informed decisions about their crop insurance needs.

Conclusion and Next Steps

Crop insurance represents a critical risk management tool that protects agricultural producers against the inherent uncertainties of farming while supporting broader food system resilience. The federal crop insurance program’s public-private partnership model has evolved since the Federal Crop Insurance Act established the foundation during the Great Depression, now covering nearly 90% of U.S. cropland through approved insurance providers.

To get started:

- Contact approved insurance providers in your area to discuss coverage options and premium costs

- Evaluate your farm’s risk profile, considering crop types, location, and historical yield data

- Review coverage deadlines and compliance requirements before planting seasons begin

FAQ (Frequently Asked Questions)

Disclaimer: Ag Optimus is not licensed to provide crop insurance and shares this information solely to support the farming community’s understanding of available risk management tools. We encourage producers to verify all details with qualified crop insurance providers. Ag Optimus is a licensed commodity broker and can offer hedging strategies designed to complement—or, where appropriate, serve as an alternative to—traditional crop insurance based on your operation’s needs.

1. What is crop insurance, and why is it important?

Crop insurance is a federally subsidized risk management tool that protects agricultural producers against financial losses from natural disasters, disease, and market price declines. It helps stabilize farm income, supports business continuity, and contributes to national food security.

2. Who administers the federal crop insurance program?

The federal crop insurance program is overseen by the U.S. Department of Agriculture’s Risk Management Agency (RMA) and managed through the Federal Crop Insurance Corporation (FCIC). Approved insurance providers sell and service policies under federal guidelines.

3. What types of crop insurance coverage are available?

The main types include Multiple Peril Crop Insurance (MPCI), which covers losses from natural disasters; crop hail insurance, a private product covering hail and fire damage; and crop revenue insurance, which protects against losses from low yields and falling prices.

4. How do premium subsidies work?

The federal government subsidizes a significant portion of crop insurance premiums to make coverage affordable for farmers. Catastrophic (CAT) coverage is fully subsidized, while higher coverage levels receive decreasing subsidy amounts, with farmers paying administrative fees.

5. Can farmers customize their crop insurance coverage?

Yes. Farmers can choose coverage levels, insured unit types (basic, optional, enterprise, multicounty, whole farm), and select policies based on individual farm yields or county averages to best fit their risk management needs.

6. What are the requirements for maintaining crop insurance eligibility?

Farmers must purchase policies before planting deadlines, follow USDA guidance on good farming practices, and comply with conservation requirements protecting wetlands and highly erodible lands to remain eligible for coverage.

7. How does crop insurance help farmers manage risk?

By providing financial protection against crop losses and revenue declines, crop insurance reduces income volatility, enabling farmers to make confident long-term business decisions and recover more quickly from adverse events.

8. Can futures and options contracts be used alongside crop insurance for risk management?

Yes. Futures and options contracts, often facilitated by a commodity broker, allow farmers to hedge against price volatility in agricultural markets. While crop insurance protects against physical crop losses and revenue declines, futures and options provide a financial tool to lock in prices or limit downside risk on commodity sales. Using both strategies together can offer comprehensive risk management by addressing both production and market price uncertainties.

9. What role does a commodity broker play in managing agricultural risk?

A commodity broker acts as an intermediary, helping farmers access futures and options markets to hedge price risk. They provide market expertise, execute trades, and offer advice on contract selection and timing. While commodity brokers do not sell crop insurance, their services complement insurance coverage by managing market-related risks that crop insurance alone cannot address.

Disclaimer: Ag Optimus is not licensed to provide crop insurance and shares this information solely to support the farming community’s understanding of available risk management tools. We encourage producers to verify all details with qualified crop insurance providers. Ag Optimus is a licensed commodity broker and can offer hedging strategies designed to complement—or, where appropriate, serve as an alternative to—traditional crop insurance based on your operation’s needs.