By Ryan Griffeth

This article is the opinion of Optimus Futures.

A marketing plan is only as good as the order that carries it out. You can know your break-even to the penny, know exactly what price works for your operation, and still end up with a fill you didn’t expect, or no fill at all, because the order you placed didn’t do what you thought it would.

Order types are not trader jargon. For a producer, they are risk-management tools. They answer three questions: immediate execution, execution at a set price, or execution only if the market moves against you. Those correspond to market, limit, and stop orders.

Key Takeaways

-

- A market order gives you certainty of execution but costs you in price. You will be filled, but you won’t know the exact execution price until it is done.

-

- A limit order ensures you get the price you want, but you sacrifice confidence in execution. It may never fill, even if the market touches your price.

-

- A stop order triggers execution; it does not guarantee the fill price. When the market reaches your trigger price, the order activates and executes at the best available price within the exchange’s protection range.

-

- For a hedger, a stop is not a “stop-loss.” You own the physical crop or the livestock. A sell stop activates a hedge when the market moves against you. It is not limiting a loss on a speculative position because you do not have one.

-

- Agricultural futures have daily price limits and reach them more often than most other markets, which affects how resting orders function.

Before the Orders: What You Are Actually Doing

If you have never traded futures, start here. A futures contract is a standardized agreement traded on an exchange: one corn contract covers 5,000 bushels, and one feeder cattle contract covers 50,000 pounds. When you hedge, you sell contracts against the grain on the cattle you own, and later buy them back to close the position. You are not signing up to deliver grain to Chicago. Nearly all hedges are offset before expiration, and the gain or loss on the futures side works against the move in your cash market.

The orders in this article are instructions you give the exchange on what to do with those contracts. You place them through a brokerage account, either yourself or by calling your broker’s desk, and each one is built from the same handful of decisions: buy or sell, how many, which month, at what price, and for how long the instruction remains in effect.

Order Types at a Glance

| Your goal | Order type | The trade-off you accept |

|---|---|---|

| Get the hedge on now. The decision is made. | Market order | You’ll be filled, but not at a price you chose. |

| Sell at a target price from my break-even math. | Sell limit (rests above the market) | You may never be filled — even if the market touches your price. |

| Put the hedge on automatically if the market breaks lower. | Sell stop (rests below the market) | Triggers at your level, fills at market. In a fast break, that’s well below your stop. |

What Is a Market Order?

A market order is an instruction to execute immediately at the best available price. You are certain to be filled; you are not certain of the price.

In a liquid market like front-month corn, on a normal day, the gap between the screen and your fill is usually small. In a thin market, a fast market, or a deferred month, it can be considerably wider. The order accepts whatever price is available rather than seeking a specific one. CME Group also offers a market order with protection, which limits fills to a predetermined price range to avoid extreme executions.

When market presence matters more than the exact price, a market order is the right choice. A producer who has decided the hedge needs to be on today is better served by a market order than by naming a price and hoping. Hedging’s worst outcome is seldom a few ticks of slippage. It is deciding to hedge and then failing to implement the hedge when the market moves.

What Is a Limit Order?

A limit order lets you set the exact price you will accept. A sell limit executes at or better than that price, but may not fill if the market moves away. You specify your desired price; the order may remain unfilled even if the market touches it.

As CME Group puts it, a limit order lets a seller define the minimum sale price, and in a fast-moving market, the order may not be filled because the price keeps moving away from it. That is the entire agreement, condensed into a single sentence.

Grain: the sell limit that works while you’re in the field

Say a corn grower has calculated his December corn target: the price level his calculations determined to be acceptable, covering his cost of production with a workable margin. That figure came from his numbers, not a hunch about the market.

He places a sell limit above the market for the portion of the crop he wants priced. Then he goes and plants. The order remains active without any emotional attachment. If the market rallies to his target, the hedge goes on at the price his calculations said was acceptable. If it doesn’t, nothing happens.

That is the point. The decision was made at the kitchen table with a calculator, on a calm day. The order implements that decision without judgment and requires no watching during a rally.

The trade-off exists and needs to be explained: a limit order can be right about the price and still not fill. Exchange matching engines prioritize resting orders by price-time priority: best price first, then the earliest order at that price. If the market reaches your level briefly and then moves away, preceding orders can take all available volume. Trading at your price doesn’t guarantee a fill.

What Is a Stop Order?

A stop order remains inactive until trading reaches your predetermined trigger price. It does not appear as a live order on the book beforehand; upon activation, it becomes executable.

The mechanics matter more than most producers realize. CME Group describes two kinds of stop orders: a stop-limit, which becomes a limit order when activated, and a stop-with-protection, which becomes a market order. A stop-with-protection activates when the market trades at or through your trigger price, and fills within a protection range.

In short: the stop price triggers the order; it does not guarantee execution at that price. The exchange’s protection range sets a minimum on fill quality; within that range, the market determines the execution price. That is not a malfunction. That is the order doing its job.

One thing that matters specifically in our markets: grain futures carry daily hard price limits, and agricultural futures hit limit-up or limit-down considerably more often than most other markets do. Locked limit-down markets may have no bids available, so a resting order there looks very different from one in a free-trading market.

Livestock — a hedge trigger, not a “stop-loss”

Here I want to be careful, because language borrowed from speculative trading can do real harm to producers.

A backgrounder owns cattle. He holds a direct position in the physical animal, with real money in feed, and his exposure is that the market falls before those cattle are sold. When he sells futures against them, that position balances his exposure rather than speculating on direction.

So when a producer places a sell stop under the feeder cattle market, it is not a “stop-loss.” It activates a hedge when the market falls below the level where adding weight no longer pays.

Think about what that means. He has done the math on what those cattle cost him to put weight on. He knows the price below which economics no longer makes sense. The stop says: if the market goes there, I want to be hedged, and I don’t want to be making that call in a panic from a tractor cab.

That is a disciplined use of the tool. It carries the caveat above, and for cattle, the limit-move rule also applies. Know both before you place the order, not after.

The Part Nobody Warns You About: Margin

Every order in this article, once filled, gives you a live futures position, and a live position requires margin: a good-faith deposit your broker holds while the position is open. If the market moves against your futures position, you will be asked to post more collateral.

Here is the part that surprises first-time hedgers. Suppose you sold futures against your corn and the market rallies. Your crop in the field is now worth more, which is good news for the operation. But the futures side is losing, and the margin calls arrive in cash this week, while the gain in the field stays on paper until you sell. The hedge is doing exactly what it was designed to do, and it can still strain your cash flow in the process. Producers who plan for that, with their lender and their broker, hedge with confidence. Producers who discover it mid-rally often abandon a sound hedge at the worst possible moment. Margin requirements vary by market and change with volatility, so ask your broker for current figures before you place the first order.

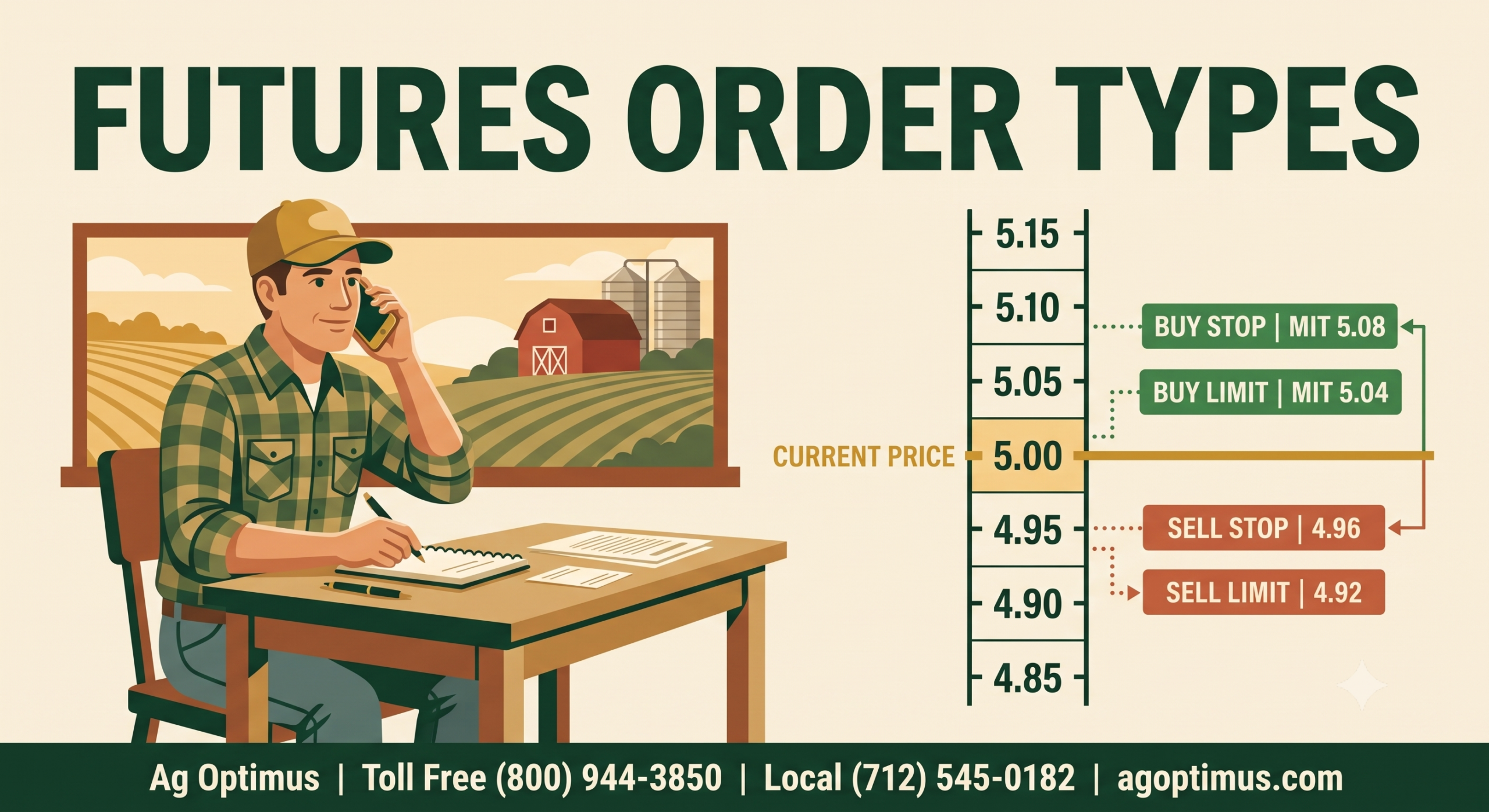

Where Each Order Rests: Corn and Cattle

The same four orders, on the two markets this article is about. Notice the shape: the green limit orders rest where the price is better for you (sell higher, buy lower), and the clay stop orders rest where it is worse, because they exist to trigger against you. Prices are hypothetical.

Read the corn ladder as the grower from the limit-order section: his sell limit at $4.70 prices a marketing tier if the rally comes to him, and his sell stop at $4.38 puts the hedge on if the market breaks before he has priced. Read the cattle ladder as the backgrounder: his sell stop at $242 is the hedge trigger sitting below the level where adding weight no longer pays. The buy orders matter later; they are how a short hedge comes off, either at a better price (buy limit) or in defense if the market runs (buy stop).

Common Mistakes Producers Make With Orders

-

- Assuming a stop guarantees the stop price. A stop order triggers execution; it does not guarantee the fill price.

-

- Using a limit order when the decision is already made. If you’ve decided to hedge, place the hedge. Tacking on a tentative price and waiting is not discipline, and markets do not wait.

-

- Placing market orders in thin overnight sessions. The screen looks the same at 2 a.m. The book underneath it does not.

-

- Forgetting a resting order is still working. A GTC order placed in April may still be active in July and will not reflect later changes, so review it before markets move.

-

- Never reviewing working orders. Positions shift, yields evolve, and break-evens move. The order on the book does not know that.

-

- Deciding the order type while the market is moving. Review your position first. Choosing mid-move is the worst possible choice under the worst circumstances.

The Anatomy of an Order: What You Say When You Call It In

An order has five parts, and a complete instruction covers all of them: the side (buy or sell), the quantity, the contract (market and month), the order type with its price, and how long the instruction stands. Spoken to a desk, it sounds like this:

“Sell three December corn at $4.70, limit, good ’til canceled.”

Side: sell. Quantity: three contracts totaling 15,000 bushels. Contract: December corn. Type and price: a limit at $4.70. Duration: it keeps working until it fills or you cancel it. Every order you will ever place is some version of that sentence, and if you call a desk with those five pieces decided, the conversation takes thirty seconds. If any piece is missing, a good broker will ask for it before anything gets placed, because the exchange needs all five.

What This Looks Like From the Desk

After two decades of working with order flow, I’ve observed that producers don’t choose the wrong order type. They simply haven’t considered which one they need.

When a grower calls to hedge, I ask whether he has decided or is waiting for a price. Those are two different orders. Once the decision is finalized, we execute. If he has a break-even figure, we place an order there and let it run. The order should follow the plan, not the other way around.

Conversations go awry when the market is moving. Deciding an order on a limit-down day often leads to poor choices. Before the market moves, decide the order’s shape — that’s what order types are for.

Talk through the order before the market is moving. We help grain and livestock producers turn marketing plans into orders that execute as intended, at a desk, with an experienced broker.

Call us toll-free at (800) 944-3850 or locally at (712) 545-0182 to speak with an Ag Optimus broker.

Frequently Asked Questions

What is the difference between a market order and a limit order?

A market order guarantees execution at the best available price, not at the exact price. A limit order sets a specific price and executes only at or better than that price, so it guarantees price but not execution.

Does a stop order guarantee I get filled at my stop price?

No. A stop order functions as a trigger rather than guaranteeing a specific price. When the market reaches your stop level, the order is activated and executed at the best available price. CME Group’s stop-with-protection limits that fill to a defined protection range, which bounds slippage, but the fill can still come in worse than your trigger in a fast market.

Is a stop order the same as a stop-loss for a producer?

No. The distinction matters because a producer who owns cattle or grain maintains a direct position in the physical commodity, so a futures hedge balances that exposure rather than speculating. A sell stop triggers a hedge if the market falls below the level where the operation becomes economically infeasible. It is not limiting a loss on a speculative position.

Can a limit order fail to fill even if the market reaches my price?

Yes. Exchange matching engines work orders on price-time priority: best price first, then whichever arrived first at that price. If the market reaches your level briefly and then moves away, preceding orders can take all available volume, so trading at your price doesn’t guarantee a fill.

What is a stop-limit order, and should a producer use one?

When activated, a stop-limit becomes a limit order rather than a market order, so it won’t execute below your set price. However, if the market gaps past that limit, it may never fill, leaving you unhedged. Hedgers should discuss this specific risk with their broker before placing a hedge.

What happens to my order if grain or cattle futures go limit up or limit down?

The agricultural futures market has daily price limits and hits those limits more often than most other markets. When a market is locked limit down, bids can disappear and stop orders may go unfilled or fill far from their trigger once trading resumes. This is one of the most important practical differences between hedging ag futures and other markets.

Do futures orders expire at the end of the session?

As a rule, yes: futures orders default to day orders and expire at the close of the session unless you specify otherwise. A GTC order remains active until filled or canceled. Producers who believe an order is still active when it has actually expired at the close can miss the move they were expecting.

Can I cancel or change a working order?

A resting order can be canceled or modified until it fills; you cannot cancel a filled order. If your circumstances change (e.g., yield estimate updates, cash sales), review your working orders promptly to ensure they still match your position.

Sources

Order-type mechanics and price-limit facts in this article are drawn from CME Group’s published exchange documentation, linked where cited above.

This material is general educational content from Ag Optimus. Ag Optimus is an introducing broker registered with the NFA and CFTC. The referenced price levels are hypothetical and used for illustration only. Order execution is subject to market conditions, and no order type guarantees a specific fill price. Exchange order-type specifications are set by the exchange and may change; confirm current specifications with your broker. Trading futures and options involves substantial risk of loss and is not suitable for all investors; you may lose more than your initial deposit. Past performance does not guarantee future results. Every operation is different; assess any strategy against your production costs, marketing plan, financial situation, and risk tolerance.

How much money do I need before I can place a hedge order?

You need a funded brokerage account with enough to cover the margin requirement for the position, which is a good-faith deposit that the exchange sets and adjusts based on market volatility. If the market moves against your futures position, you will be asked to post additional cash margin, even when the hedge is performing its job. Ask your broker for current margin figures for your market before placing the first order, and plan that cash flow with your lender.