Prices are mixed overnight with corn prices lower on better -than -expected ratings, and a poor inspections report yesterday that suggests exports may not achieve USDA projections. Beans are firmer on a steady rating, but drier conditions moving into the following week. There is also chatter that China purchased a combination of US and Brazil bean cargoes last week. This outlook could favor buy bean and wheat trade/sell corn into the report. Spreading forward of September contracts continues. The Farmer Survey done in August will also be out soon. There is some harvest in the southeast.

The UN climate report sounded the alarm on human greenhouse activity yesterday which sent prices to their lows, with crude oil impacted the most. Though an oilshare correction was the result of headlines yesterday, soyoil futures are showing more stability this morning. Crude oil prices firm from yesterday’s losses.

STORIES

Heavy rain in France, the EU’s largest wheat producer, has added to worries about global wheat export supplies as harvest prospects have also deteriorated in North America and Russia. Ships have been waiting for up to a month at France’s biggest grain port to load wheat for Algeria as a rain-hit harvest forced exporters to compete for a reduced supply.

WEATHER – Good rains were noted over many parts of the country over the past weekend, but moving forward there is a limited amount of moisture and warming temperatures. Would look for this trend to have the most impact on beans, with corn a follower as many believe the crop has already gone through successful pollination at least in the eastern cornbelt. Dry conditions will be in the Dakotas, Minn., western Iowa, while ECB sees normal weather.

Black Sea conditions remain mostly dry, and in Argentina as well.

REPORTS

Crop progress

beans: 60% good/excellent, unchanged from wk ago. Illinois, Missouri, and Wisconsin improved the most. Indiana, the Dakotas, and Nebraska conditions were lower. Blooming: 91% vs. 86%. Setting pods: 72% vs. 58%.

corn: 64% good/excellent, up 2% with an 11% surge in Illinois. Missouri and Wisconsin ratings were also good. Silking: 95%. Dough stage: 56%. Dented: 8%.

winter wheat: 95% harvested vs. 91% yr ago.

Spring wheat: ratings improve 1% to 11% good/excellent. Harvest: 38% complete.

ANNOUNCEMENTS

Brazil’s CONAB cut its bean forecast to 82.42 mln tns vs. 86.69 in July, saying it could be lower if shipments fail to pick up in coming months. Conab sees Brazil’s corn exports at 23.5 mln tns this season, and imports unchanged at 2.3 mln tns. The Safrinha crop is forecast for 20/21 at 60.322 mln tonnes vs. 66.970 mln tonnes in July, and vs. 75.053 mln tonnes yr ago.

Brazil gov. data shows bean exports month-to -date average in AUgust 276 tmt/day vs. 278 tmt /day yr ago.

Brazil’s Aboive forecast 2021 bean crushing volumes at 46.5 mln mt, down from 46.84 mln mt yr ago, attributed to uncertainty of the biodiesel mandates. They forecast bean exports at 86.7 mln mt vs. 82.9 mln mt yr ago.

China’s customs data forecast July bean imports at 8.67 mmt, down 14% from yr ago due to negative crush margins.

DELIVERIES

August:

soyoil: 1

Calls are as follows:

beans: 4-6 higher

meal: 2.80-3.00 higher

soyoil: 4-9 higher

corn: 2 1/2-3 lower

wheat: 2-3 higher

Outside markets feature a quieter outlook with the Dow off 20 pts, and crude oil prices trading up to $68.05/barrel. THe US dollar firms to 93.0.

Tech talk: November bean prices continue to consolidate from $13.20 – $13.90, but now appear to be well bid for the day and attempting to establish support once more for a trade back towards the pivot level at $13.50. A solid push above the 100 day moving average at $13.40 will keep the market well bid, and the chart appears ready to see higher values. The December meal chart has now established very good support at $350.00, having had multiple chances to trade lower. The price action is sideways from $350.00 to $375.00, and think we see upside follow-through. December soyoil breaks the 60c level which opened the door to a trade down to 5937c. Prices have to prove that this level is an overall low, but if we take out 59c next target is 58c, as there is little back support to help.

December corn remains a trapped $5.40 to $5.65 range. The 100 day moving average crosses at $5.42, and any break of this level opens the door to further liquidation. Approaching lines of support continuously is never a sign of strength, though the overall trend remains weak. Looks like the USDA report may be the item to send this one way or the other. The December wheat chart still remains positive having posted new highs at $7.49 and double lows at $7.22. The pattern still appears more friendly for wheat than negative, as prices are retreating from the newest high, but the congestion zone could be a bull flag, and that is more friendly than not.

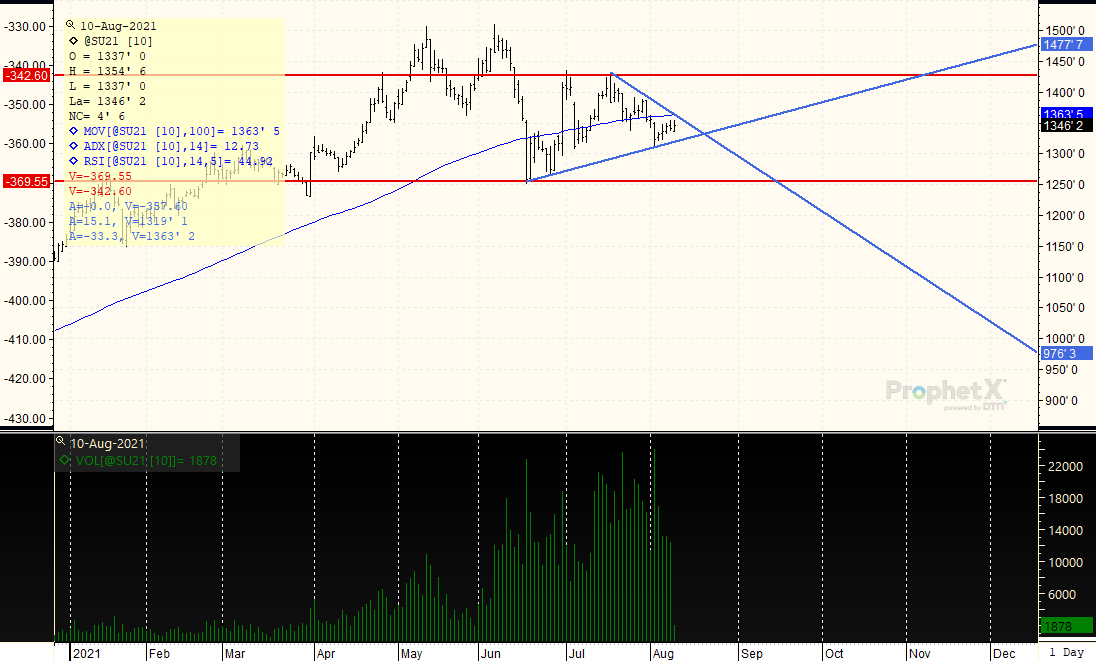

SEPTEMBER BEANS: Prices are wedged sideways from $13.20 to $13.80. Both the 100 day moving average and trendline resistance converge at $13.55/$13.60, which is stiff resistance. THe ADX is weak at 12, as the market cannot seem to make up its mind which way to go. Support at the lows is stronger than resistance at the top, though until prices break out to one side or the other could continue to see the market operate in a comfort zone from $13.20 – $13.75, pivoting around the $13.50 level. Stiff resistance is at $13.50, and could be difficult to overcome given the lack of direction and overall volumes.

Receive Relevant and Timely Grain Market Reports that Matter!

Get updated twice a week with concise, direct information that you can use in grain trading, marketing, and farm management

Better yet, become a customer and get DAILY updates, fundamental, and technical, sent straight to your Inbox! Contact Us now to get started.

[su_button url=”https://agoptimus.com/contact-us/” target=”blank” style=”flat” background=”#efb82d” size=”8″ wide=”yes” center=”yes” radius=”0″ icon=”icon: external-link”]Contact Us[/su_button]

RISK DISCLAIMER: Trading in commodity interest products such as futures, options and otc swaps entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources. You may lose all or more of your initial investment. Opinions, market data, and recommendations are subject to change at any time. The placement of contingent orders by you or broker, or trading advisor, such as a stop-lossor stop-limitorder, will not necessarily limit your losses to the intended amounts, since market conditions may make it impossible to execute such orders. Long options strategies could lose their entire premium plus transactional costs. Short options strategies entail unlimited risk of loss plus transactional costs. The information presented represents the opinion of Ag Optimus. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance. Futures prices factor in the seasonal aspects of supply and demand. This communication may cite historic data and should not be taken to mean certain trades can produce dramatic profits year in and year out. This information does not imply customers have or will experience profits based on seasonal trades or trade data. All information, communications, publications, and reports, including this specific material, used and distributed by Optimus Futures, LLC (“Optimus”) shall be construed as, or is in the nature of, a solicitation for entering into a derivatives transaction. Optimus does not distribute research reports, employ research analysts, or maintain a research department as defined in CFTC Regulation 1.71. This email may include information produced by third parties. Material not labelled Optimus Futures should be considered to be third-party, and is provided for informational purposes only. Third-party material is from sources believed to be reliable, but its accuracy is not guaranteed by Optimus Futures. Optimus Ag and Ag Optimus are registered dbas of Optimus Futures LLC [NFA ID 0481133] CONFIDENTIALITY NOTICE: Privileged/Confidential information may be contained in this message. If you are not the intended recipient, please notify the sender immediately and you must not use the message for any purpose nor disclose it to anyone. Communications on all mediums may be recorded.